Oklahoma's Commercial Construction Market Is Entering a Historic Expansion Cycle

Overview

The Oklahoma City MSA is on track for one of the most sustained construction booms in its history. A $900 million Thunder arena, a $2.7 billion GO bond, a $1 billion MAPS 4 program, $9 billion in Google data center investment, and an estimated $1.5–$2.5 billion in annual tribal construction spend have converged into a pipeline that is growing at three to four times the national rate. For developers, owners, and contractors operating in the Oklahoma market, understanding what's driving this cycle — and where the pressure points are — has real strategic value.

A $4.8 Billion Market Growing Faster Than the Nation

The OKC MSA tracked $4.47 billion in total contract value in 2024 (Dodge Construction Network), 9% above 2023. Dodge projects 2025 at $4.79 billion — historically robust even though it represents a slight moderation from 2024's peak. The forward-looking data is more striking: Dodge's 2026 forecast calls for +12% total growth in the OKC MSA against 0% nationally, with non-residential construction specifically projected at +22%. The OKC metro accounts for roughly 37% of Oklahoma's population and approaching 40% of state GDP, making it the clear center of gravity for this expansion.

Construction employment in the OKC MSA grew 7.1% year-over-year in 2025 — the highest-growing employment sector in the metro — with a further 1.7% forecast for 2026. Statewide, Oklahoma added 3,100 construction jobs (3.7%) in 2024, placing it among the top five states nationally for construction employment growth. The unemployment rate in OKC has remained below 4% for 52 consecutive months, ranking among the top 10 lowest for large metros exceeding one million in population.

The top-gaining non-residential sectors in the OKC MSA during 2024 were manufacturing and science labs, government, water supply systems, education, and retail. Non-building infrastructure is the single biggest growth driver, with Dodge projecting a +72% increase in 2025 alone — fueled by federal IIJA funding and turnpike construction.

Where the Spending Is Going

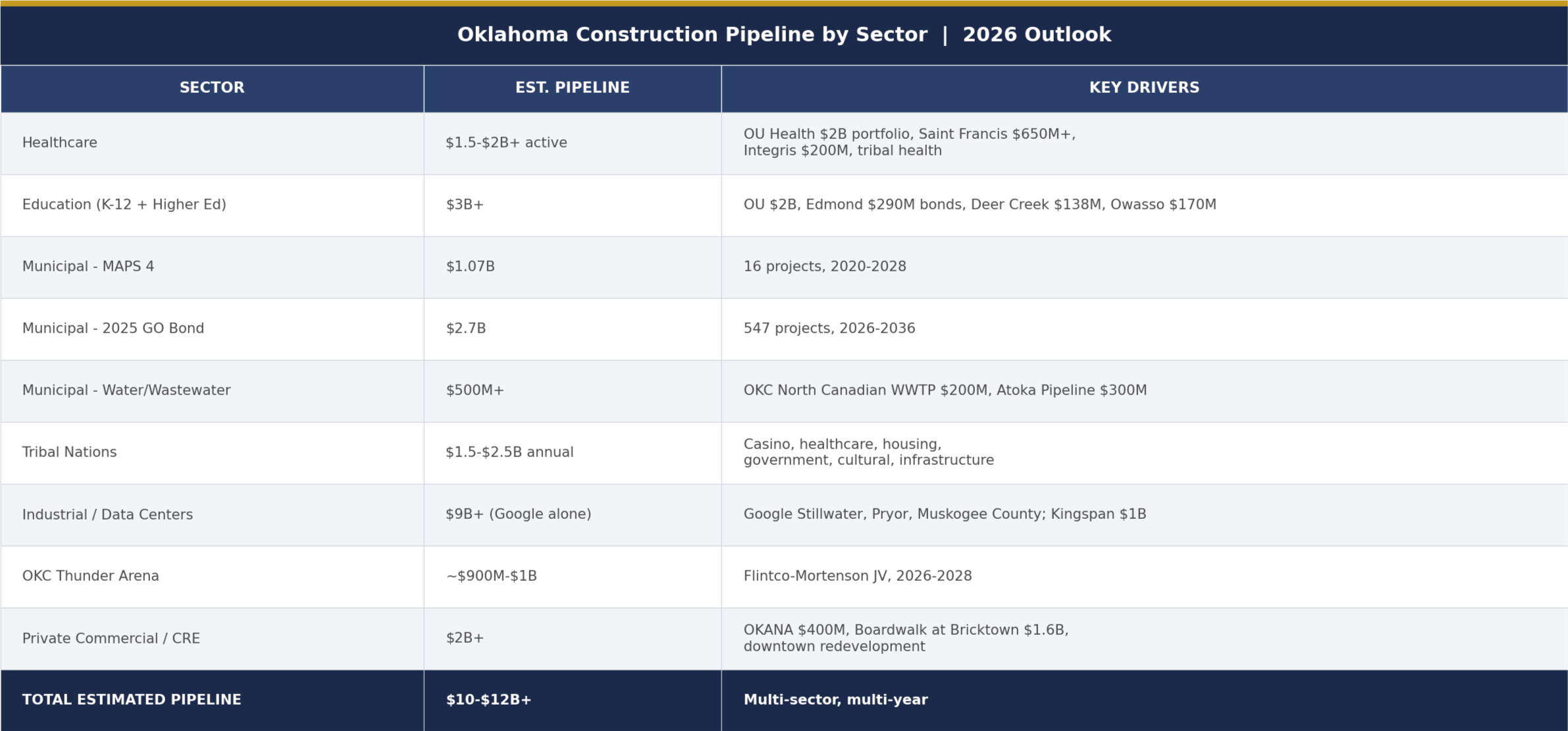

Oklahoma’s 2026 Commercial Construction Pipeline Outlook by Sector

Federal Infrastructure Money Is Reshaping the Pipeline

Oklahoma has been allocated $6.4 billion in total federal infrastructure funds — IIJA, IRA, and CHIPS combined — as of mid-2024. Federal highway formula funding alone totals $4.6–$4.7 billion over five years (FY2022–2026), with FY2024 apportioning $945 million for roads, bridges, and critical infrastructure across 12 formula programs. Key IIJA allocations to Oklahoma include:

Key IIJA Allocations to Oklahoma

● $797.4 million for broadband (BEAD Program)

● $506 million for water and wastewater infrastructure

● $352 million for public transit

● $137 million for airports

Notable individual funded projects include the $85 million I-44/US-75 Corridor (Mega Projects grant), a $11.5 million Bridge Investment Program covering seven Northwest Oklahoma bridges, and $105+ million in EPA water infrastructure improvements. ODOT's Eight-Year Construction Work Plan encompasses approximately $9 billion in highway construction and safety projects from FY2025 through FY2032, heavily leveraging federal match dollars.

For the tribal construction market specifically, the Bipartisan Infrastructure Law allocated $3.5 billion nationally for Indian Health Service construction from 2022–2026 ($700 million annually for sanitation facilities). HHS Secretary Kennedy also announced an additional $1 billion in existing resources directed toward priority IHS healthcare facility infrastructure beginning FY2027. Federal road funding to Oklahoma tribes runs approximately $67 million annually through the DOT Indian Reservation Roads Program.

Three Mega-Projects Defining the Next Decade

MAPS 4

OKC's MAPS 4 is a $1.07 billion program funded by a temporary one-cent sales tax running from April 2020 through approximately 2028, with actual revenue already exceeding the original $978 million projection. The program encompasses 16 projects, roughly 70% of which are directed toward human and neighborhood needs. Projects currently in construction include a 68,000 SF animal shelter ($42M), the Innovation District Phase 1 ($76.7M), sidewalks and bike lanes ($96.5M in phases), and the Bus Stop Improvements program ($11.2M). The centerpiece — a new Multipurpose Stadium budgeted at $121 million (up sharply from $41M originally), designed by Populous for 10,000+ soccer and 20,000 concert capacity — breaks ground spring 2026 with a January 2028 opening target.

The New Thunder Arena

The new OKC Thunder Arena is the single largest construction project in the metro's history at $900 million to $1+ billion. The Flintco-Mortenson joint venture was selected in March 2025 as construction manager. Demolition of the former Cox Convention Center wrapped by end of 2025, with construction beginning Q1 2026 and a target opening of late summer 2028. The arena features a 360-degree glass curtain wall and is funded by a 72-month penny sales tax beginning after MAPS 4 concludes, supplemented by $78M from MAPS 4 and $50M from Thunder ownership.

The $2.7 Billion GO Bond

Perhaps the most consequential long-term signal is the $2.7 billion OKC General Obligation Bond approved October 14, 2025 — the largest GO bond in the city's history. It encompasses 547 projects across 11 propositions:

$1.35B+ for streets and bridges

$414M for parks and recreation (including Chickasaw Bricktown Ballpark, Civic Center Music Hall, USA Softball Complex, and RIVERSPORT)

$175M for economic and community development (including $50M for affordable housing)

$190M for drainage, $140M for fire stations

$104M for transit, and $78M for police and courts

Construction begins in 2026 and runs through approximately 2036 — a decade-long continuous pipeline.

The Tribal Nation Market: $1.5–$2.5 Billion Annually

Oklahoma's 39 federally recognized tribes — more than any other state — generated $23.4 billion in total economic impact in 2023, with Class III gaming revenue reaching $3.47 billion in FY2024 (tribes paid a record $210.2 million in state exclusivity fees). An estimated $1.5–$2.5 billion flows into construction annually across casinos, healthcare, housing, government buildings, cultural centers, and infrastructure. In 2015 alone, tribal gaming operations spent $363 million on capital improvements, creating 2,768 construction jobs.

The Six Largest Tribal Spenders

Chickasaw Nation ($1.25B+ estimated Class III revenue, 14,000+ employees, $3.7B annual economic impact) recently opened the $400M OKANA Resort and is actively investing in an OKC soccer stadium, child development centers, housing programs, and a new 72-bed Newcastle hospital.

Choctaw Nation (FY2026 budget: $2.6 billion, with $600M reinvested in the reservation) built the $238M Choctaw Landing and announced the $6 billion Preston Harbor mega-development — a long-term project that will be one of the largest tribal construction programs in the country.

Cherokee Nation (450,000+ citizens, 11,000 employees) has an $800M+ healthcare construction pipeline including the $470M W.W. Hastings Hospital replacement and the $400M Claremore Health Center.

Muscogee (Creek) Nation recently opened the $100M Coweta Casino Hotel and the $69.8M Lake Eufaula Casino.

Citizen Potawatomi Nation built the FireLake Casino & Hotel and an 82,000 SF tribal administration headquarters, with additional capital projects in the OKC metro area.

Osage Nation completed casino-hotel expansions in Tulsa ($160M), Bartlesville, and Pawhuska.

Why Tribal Procurement Stands Apart

Tribal nations are sovereign governments not bound by Oklahoma's Public Competitive Bidding Act. Each tribe establishes its own procurement policies, generally operating under a hybrid model that combines competitive elements with strong relationship preferences. The Tribal Employment Rights Ordinance (TERO) system — approximately 11 programs operate in Oklahoma — gives preferential treatment to Indian-owned businesses and imposes 1–4% compliance fees on construction contracts. Contractors must file TERO compliance plans, give preference to qualified Indian workers, and submit certified payroll reports.

This procurement structure inherently advantages firms that invest in long-term tribal relationships over those competing solely on price. It also means that sovereign tribes can — and regularly do — select delivery methods based purely on what works best for the owner: CMAR, design-build, progressive design-build, or traditional GC. No state statute constrains them. That flexibility is a significant factor in why alternative delivery method adoption is more advanced in the tribal sector than in any other Oklahoma owner category.

Alternative Delivery Methods Are Reshaping Oklahoma Procurement

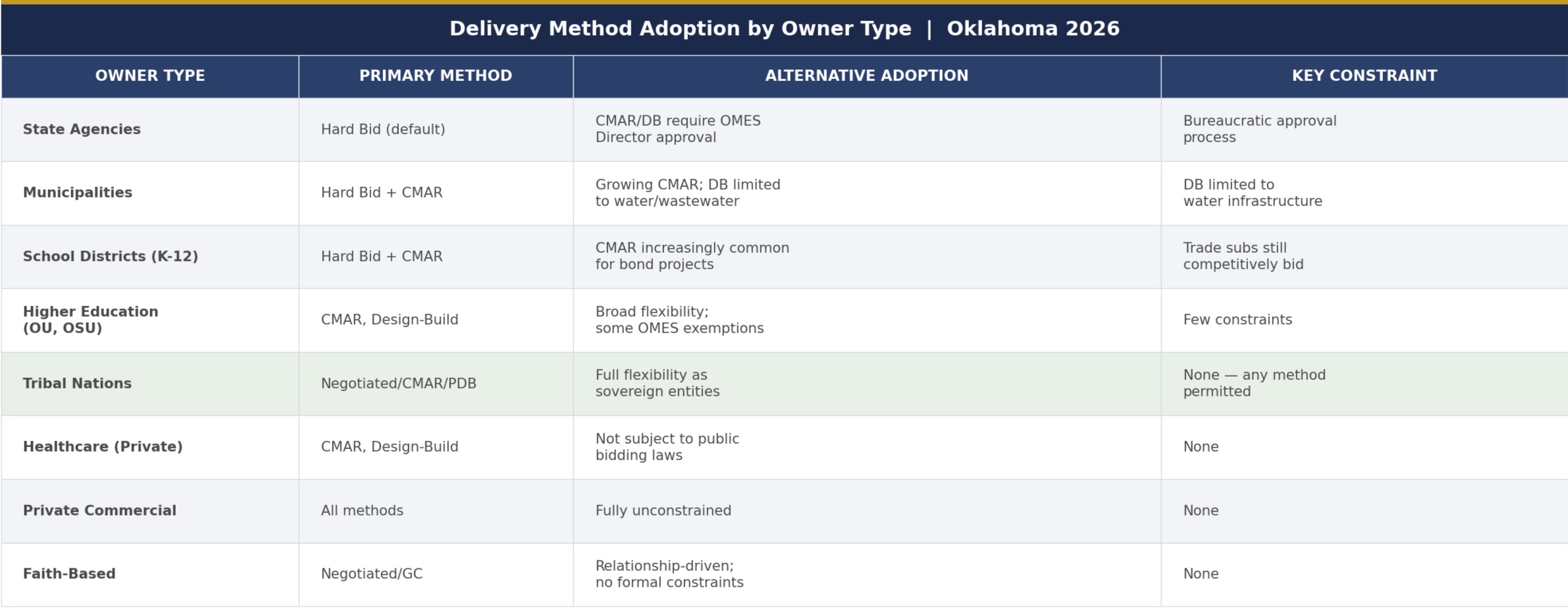

The Current Delivery Mix

Oklahoma's procurement landscape is shifting, though hard bid still dominates by volume. Hard bid (design-bid-build) represents an estimated 45–55% of non-residential projects, driven by the Public Competitive Bidding Act's default requirement of lowest-responsible-bidder awards for contracts exceeding $100,000. CMAR has grown to an estimated 25–30% market share and is the leading alternative method expressly authorized for all political subdivisions. Design-build accounts for approximately 15–20% but faces statutory constraints — it is explicitly authorized for public buildings only for water and wastewater projects at the municipal level. Progressive design-build remains at an estimated 2–5%, primarily in tribal and private-sector work.

The OMES Construction and Properties division maintains a registry of qualified construction managers: 74 registered firms as of June 2024, growing to approximately 82 by March 2025, with roughly 40 firms also holding design-build registrations.

Owner Adoption by Sector

Oklahoma’s Delivery Methods & Adoption by Owner

The West South Central region (Oklahoma, Texas, Arkansas, Louisiana) is projected to experience an 8.8% CAGR in design-build adoption through 2028 — the highest growth rate among all U.S. regions. Nationally, design-build is projected to represent over 47% of all U.S. construction spending by 2028, totaling $2.6 trillion over five years. Oklahoma's legal framework trails the national trend for public work, but the tribal and private sectors — which constitute a large share of the state's construction volume — are unconstrained and moving rapidly.

The Labor Market: Tight and Getting Tighter

Oklahoma has only 66 available workers for every 100 open construction positions, making it one of the tighter labor markets nationally. Average hourly earnings in Oklahoma construction sit at approximately $32/hour — well below the national average of $39.33 — a dynamic that creates downward pressure on labor supply relative to higher-paying regional markets.

The construction industry nationally needs 439,000 additional workers in 2025. Oklahoma's aging workforce and population demographics project a shortage of approximately 20,000 construction workers by 2028. The most acutely scarce trades are electricians, pipefitters, heavy equipment operators, and HVAC technicians — precisely the trades needed in volume for the infrastructure and commercial pipeline described above.

For owners and developers planning projects in this environment, early engagement with contractors and locked-in trade contractor relationships are increasingly important. Subcontractor capacity, not just general contractor capacity, is a real scheduling constraint.

Material Costs: Tariffs Are Accelerating an Already Rising Curve

Nonresidential construction input costs finished 2025 up 3.2% year-over-year, but the January 2026 annualized rate surged to 7.1% — a significant acceleration. The tariff regime is the primary driver.

Current tariffs include 50% on steel and aluminum, 35% on non-USMCA Canadian goods, 25% on non-USMCA Mexican goods, and a 50% tariff on copper (implemented August 2025). The downstream material cost impact is significant: steel mill products PPI jumped 17% in full-year 2025, aluminum mill shapes surged 30.5%, and copper wire and cable jumped 22%. Cushman & Wakefield estimates tariffs increased construction material costs by 9% relative to 2024 averages, translating to approximately 4.6% in total project cost increases.

Oklahoma is particularly exposed given the prevalence of steel-intensive commercial and industrial construction and the state's historically lower-margin market environment. Material escalation clauses in contracts are becoming standard practice across the industry — owners and contractors alike are building price-adjustment mechanisms into GMP and lump-sum agreements that would have been unusual five years ago.

The Bonding Market Is Tightening

The surety market is under pressure. Corporate insolvencies hit a 14-year high in 2024, and sureties are becoming more selective as tariff uncertainty compounds thin subcontractor margins. Bonding capacity generally runs 10–20x adjusted working capital, meaning that for most small and mid-size Oklahoma contractors, access to larger projects is constrained less by technical capability than by the size of their balance sheet. CPA-audited (versus compiled) financial statements significantly increase bonding limits — a detail that matters more in the current surety environment than it did several years ago.

For owners evaluating bids from smaller contractors, it is worth explicitly confirming single-project and aggregate bonding capacity before award — particularly as that capacity may be stretched across multiple projects simultaneously in a hot market.

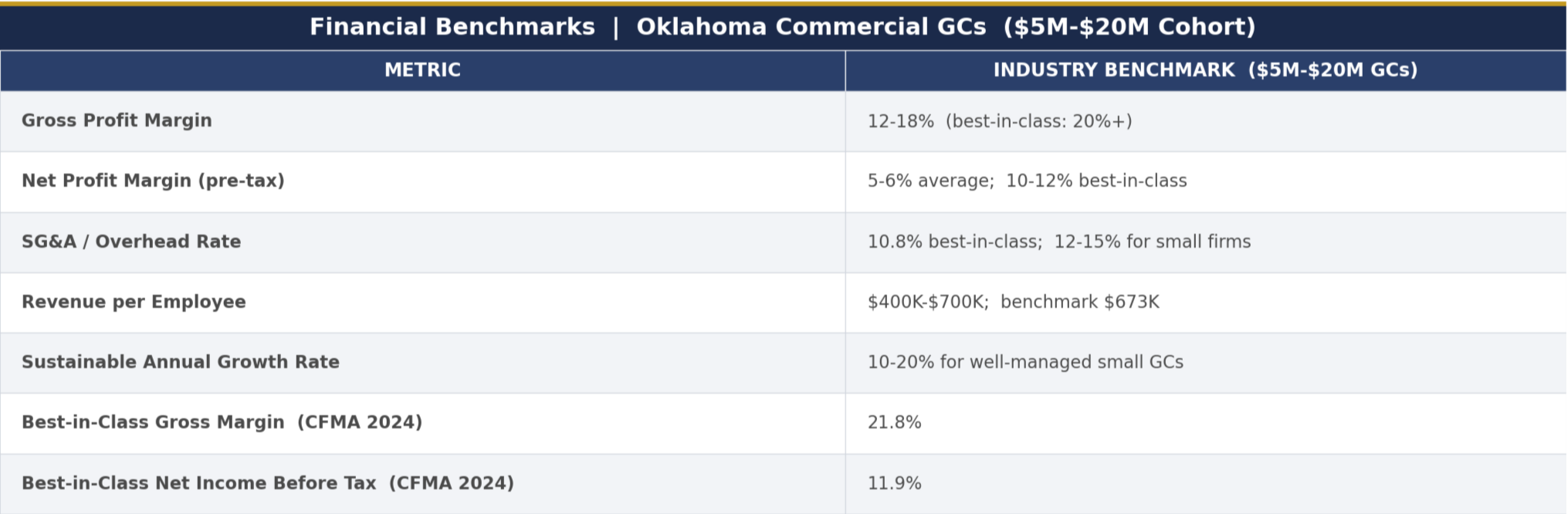

Financial Benchmarks for the Oklahoma Market

Source: CFMA 2024 Annual Financial Survey — $5M–$20M General Contractor Cohort

Oklahoma GCs Financial Benchmarks by 2024 Data Comparison

The CFMA 2024 Construction Financial Benchmarker (1,290 companies) reports best-in-class contractors achieve a gross profit margin of 21.8% and net income before tax of 11.9% — five percentage points above the average. The "10-10 Rule" (10% overhead + 10% profit = 20% total markup) remains the industry baseline, though alternative delivery firms — those selling preconstruction expertise, risk management, and collaborative process — should command premiums above hard-bid margins.Call-to-Action

Last but not least, place a call-to-action at the bottom of your blog post. This should be to a lead-generating piece of content or to a sales-focused landing page for a demo or consultation.

Three Structural Realities Shaping the Next Three Years

1. Capacity constraints are real and project-driven.

The Thunder Arena alone will absorb substantial contractor bandwidth from 2026 through 2028. The GO Bond's 547 projects, the MAPS 4 remaining work, ongoing tribal capital programs, and a healthcare sector with $1.5B+ in active projects are all competing for the same pool of labor, subcontractors, and construction management capacity. Projects that might have had multiple competitive bidders in 2022 will increasingly face thinning contractor fields — a market condition that favors early owner engagement and negotiated delivery over public bid.

2. Alternative delivery adoption is accelerating in the owner categories where Oklahoma's legal constraints don't apply.

Tribal nations, private healthcare systems, private developers, and faith-based organizations — taken together, a substantial plurality of Oklahoma's construction volume — are unconstrained by the Public Competitive Bidding Act. CMAR and design-build are not alternatives to consider in this segment; they are rapidly becoming the standard. Owners in constrained public categories (municipalities, school districts) who haven't yet built CMAR procurement experience should be investing in it now.

3. The tribal construction market is the fastest-growing owner segment with the least contractor saturation at the mid-size project tier.

The Big Six tribal nations dominate headlines with $100M–$400M+ projects, but the majority of Oklahoma's 39 federally recognized tribes are building community centers, clinics, administrative buildings, wellness centers, child development centers, housing, and infrastructure in the $2M–$25M range. This work is relationship-based, sovereign-procured, and benefits from CMGC and collaborative delivery in ways that are well-documented nationally.

Our Final Take

The Oklahoma commercial construction market is not experiencing a typical regional uptick. It is in a convergence of federal investment, municipal commitment, tribal capital deployment, and private sector confidence that, taken together, constitutes a generational expansion cycle.

The capacity constraints — labor, materials, bonding, qualified contractors — are real and will shape how this pipeline gets built. Owners who engage early, structure contracts with appropriate escalation provisions, and build genuine contractor relationships before they need them are the ones best positioned to deliver projects on schedule and on budget over the next decade.

Data sources: Dodge Construction Network (2024–2026); CFMA 2024 Annual Financial Survey; DBIA National Design-Build Market Study; U.S. Department of Transportation IIJA allocations; Indian Health Service FY2022–2027 construction budgets; ODOT Eight-Year Work Plan FY2025–2032; National Indian Gaming Commission FY2024; ENR Top 400 Contractors; OMES Construction Manager Registry; Cushman & Wakefield 2025 Construction Cost Report. Revenue figures for privately-held firms are estimates derived from ENR rankings and industry intelligence.

Stronghold Construction - Oklahoma City